7 million student loan borrowers will begin receiving deadline notices on July 1, 2026, after the Department of Education moves to wind down the SAVE income-driven repayment plan, according to Business Insider. Those who miss a 90-day window to choose a replacement plan will be automatically placed on either the standard repayment plan or the new tiered standard plan, both of which carry higher monthly payments than existing income-driven options.

What Triggered the Deadline

President Trump's elimination of SAVE set this timeline in motion. SAVE had offered borrowers lower monthly payments and a shorter path to debt relief. Beginning July 1, the department will send email notifications to enrolled borrowers outlining the 90-day window to select a qualifying replacement. An email reviewed by Business Insider stated plainly, "Your monthly payment amount will most likely go up if you are enrolled in either of these plans."

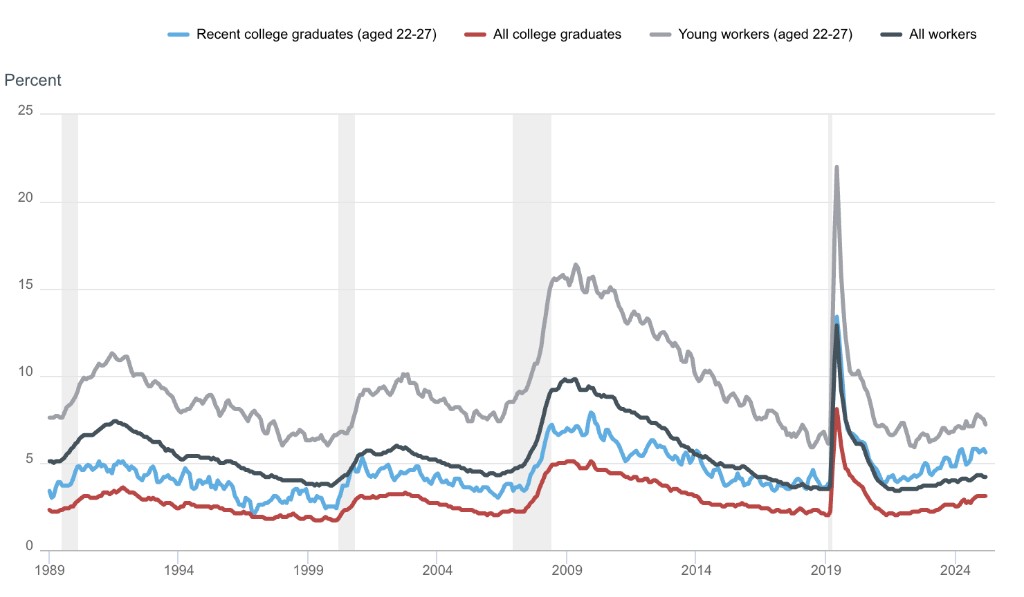

This shift arrives at a difficult moment for recent graduates. The Federal Reserve Bank of New York reported that the unemployment rate for recent college graduates stood at about 5.7% in the first quarter of 2026, while the underemployment rate remained high at 41.5%. Those labor-market conditions make rising monthly loan bills especially consequential for younger households managing tight budgets.

Unemployment Rates for Recent College Graduates vs. Other Groups

Source: New York Fed

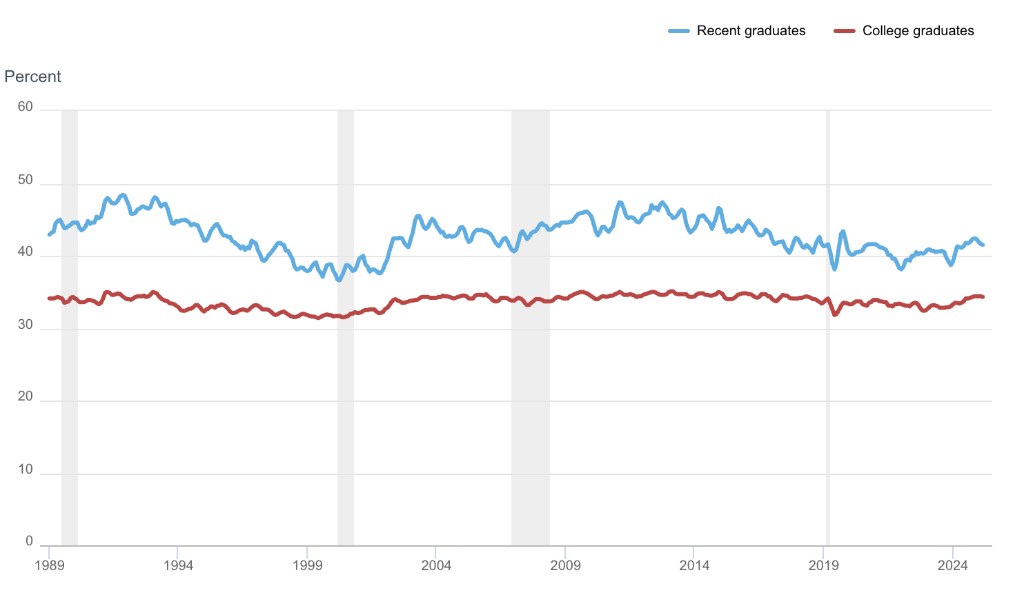

Underemployment Rates for Recent College Graduates

Source: New York Fed

The New Plans and What They Cost

Two replacement options become available after July 1. The tiered standard plan requires borrowers to repay loans in full over a period tied to their principal balance, with a minimum payment of $50 a month. The Repayment Assistance Plan, or RAP, calculates monthly payments based on adjusted gross income, but it is more expensive than existing income-based plans because it does not carve out a borrower's monthly living expenses before setting the payment amount. Some borrowers have already reported that their payments are projected to surge by hundreds of dollars under RAP, which the department positions as the more affordable new option.

Federal student loan defaults have already been returning to pre-pandemic levels after a prolonged payment pause, as tracked by researchers at the Federal Reserve Bank of New York. That context underscores the financial stakes: households absorbing sharply higher monthly payments are also navigating a credit environment where missed payments carry serious long-term consequences.

What Democrats Are Asking

More than 60 Democratic lawmakers wrote to the Department of Education urging it to automatically place SAVE borrowers in the lowest-cost plan available to each borrower if they do not act before their deadline. "To mitigate the potentially devastating financial impact of this transition, ED should automatically enroll every borrower currently in the SAVE forbearance in the lowest cost repayment plan currently available to that borrower," the letter stated. The department has not publicly committed to that approach. Nicholas Kent, the department's under secretary, said in an April press release that the changes are designed to prevent borrowers from taking on "unmanageable debt levels that they may never be able to repay."

Source: Federal Reserve Bank of New York

Additional Changes Affecting Household Borrowing

The repayment transition is not the only shift hitting student-loan households. New provisions in Trump's "big beautiful" spending legislation will introduce borrowing caps on advanced degrees and change the amounts parents can borrow for their children's education. Borrowers are not required to act until they receive their individual notices, but waiting until the last moment of the 90-day window carries the risk of missing the deadline entirely and landing on the more expensive standard or tiered standard plan. The Consumer Financial Protection Bureau maintains resources on repayment options that borrowers can use to compare plans before making a selection.

With the underemployment rate at 41.5% for recent graduates and defaults already climbing, the financial pressure on borrowing households is real and measurable as this July 1 clock starts.

Final Thought: For the 7 million households on SAVE, the 90-day window is the single most important personal finance deadline of the summer. Missing it means a higher monthly payment, likely by hundreds of dollars, with no automatic fallback to an affordable plan.