A New Debt Product Emerges From the Housing Crunch

More than 109 million Americans face a monthly rental bill, and reporting by the Financial Times finds fintech lenders are now explicitly targeting that group with rent now, pay later products. The pitch borrows from the buy now, pay later playbook that reshaped retail spending: a lender covers the full monthly payment to a landlord, then collects repayment from the renter in two or more installments, sometimes with fees or interest attached.

The structure works as a cash-flow tool for renters living paycheck to paycheck. For a household already stretched thin, spreading one large due date across smaller payments can feel like relief. It also introduces a new recurring debt obligation on top of rent itself, without lowering the total cost of housing.

Source: Pexels

Housing Costs Remain a Dominant Household Burden

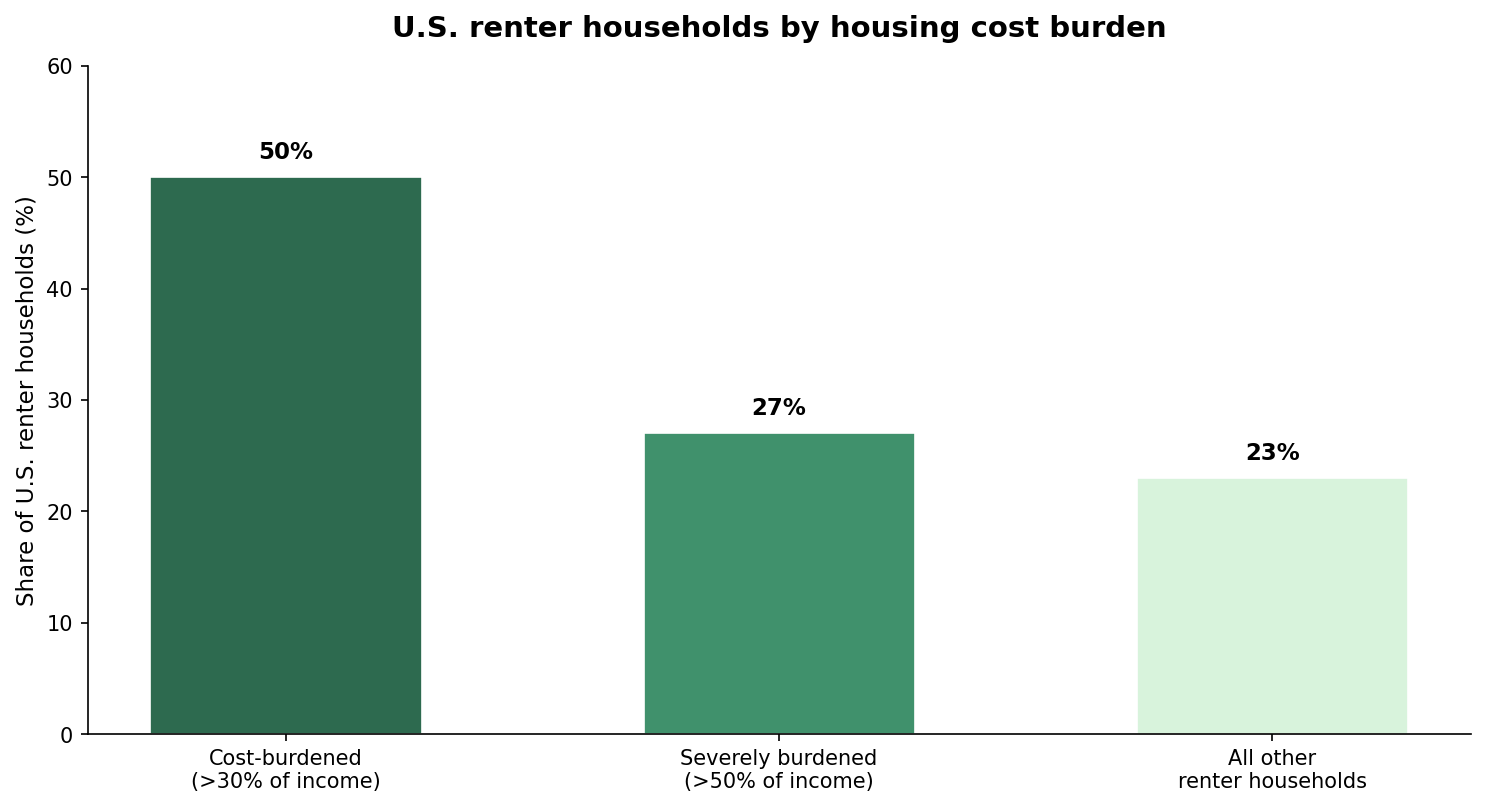

The growth of rent now, pay later products did not happen in a vacuum. According to a Protect Borrowers investigation, more than half of US renter households, roughly 22 million households covering about 55 million people, are rent-burdened, meaning they spend more than 30% of income on housing. More than 12 million households, about 30 million people, spend over half their income on shelter.

The squeeze shows up in monthly budgets, not just averages. For renter households earning $30,000 or less, the median amount left after paying housing costs is just $250 per month to cover food, transportation, and everything else, according to the same report. Zillow's March 2026 rental report puts the typical US asking rent at $1,910, up 1.8% year over year, and estimates a household now needs to earn about $76,400 per year to comfortably afford that payment, 35% more than the income required before the pandemic.

As the chart below shows, cost-burdened and severely burdened households together account for roughly three-quarters of the renter population, leaving limited room to absorb fees from installment products layered on top of rent.

Source: Protect Borrowers (Rent Now, Pain Later), citing HUD/JCHS estimates

Major BNPL Players Are Moving Into Rent

The rent now, pay later model is expanding beyond niche fintech startups. Payments Dive reports that Affirm, one of the largest buy now, pay later companies, will soon offer installment loans to renters through a partnership with Esusu, a tenant financial-services platform. Consumer advocates note that Zip already offers BNPL for rental payments, but Affirm is the first BNPL provider of its size to enter the space.

Under the Esusu pilot, eligible renters approved by Affirm can split rent into two equal biweekly payments at 0% APR, with no hidden or late fees and no interest-bearing loans offered as part of the program, according to an Affirm spokesperson cited by Payments Dive. Affirm said it underwrites each application individually and blocks new borrowing when a prior month's balance is still outstanding.

That zero-fee structure differs from other rent-splitting products. The Protect Borrowers report documents membership fees, bill-payment charges, and processing costs on some platforms that can push effective annual borrowing rates above 180% in certain cases, well into payday-loan territory. A Consumer Financial Protection Bureau study cited in industry coverage found late fees are assessed on 4.1% of buy now, pay later loans, a figure lenders cite as evidence of low default rates but that critics say understates households juggling multiple automatic withdrawals.

What Renters Should Understand Before Signing Up

The core risk with rent now, pay later is that it does not reduce the cost of housing. It restructures the timing of payment while potentially adding fees or interest, meaning a renter who uses the product every month could end up paying meaningfully more annually than the face value of their rent. The Financial Times notes these products are aimed at consumers already squeezed by housing costs, a group with limited cushion to absorb additional charges if repayment becomes difficult.

Consumer advocates raise a practical question: what happens when next month's rent is due while last month's installment is still being repaid? April Kuehnhoff, a senior attorney at the National Consumer Law Center focused on tenant protections, told Payments Dive that using short-term installment loans for a recurring bill like rent may only deepen the cycle of debt.

Regulatory scrutiny of buy now, pay later products has grown in recent years, and rent now, pay later sits in a similarly complex space where consumer protection rules may not be fully settled. Borrowers should confirm whether a product reports to credit bureaus, what fees apply for late or missed payments, and whether the lender is licensed in their state.

Final Thought: Rent now, pay later loans offer short-term cash-flow relief but add a new debt layer to one of the largest fixed costs in any household budget, making it essential for renters to fully understand total costs before enrolling.