Installment Loans Are Moving Into the Grocery Aisle

Buy-now-pay-later financing, once tied to discretionary purchases like electronics and clothing, is showing up on gas and grocery receipts. MarketWatch reports that Americans are routinely using BNPL to cover essentials that households used to pay from checking without a second thought. The shift lands as pump and supermarket prices stay elevated after gasoline reached $4.47 per gallon nationally in May, according to U.S. Energy Information Administration data cited in recent consumer-spending coverage.

Source: Pexels

Survey Data Shows BNPL Spreading to Necessities

Household surveys point to a sharp change in how installment credit is used. The Federal Reserve Bank of New York finds that 29% of BNPL users now report using installment loans for groceries, more than double the share from two years ago, while 47% made at least one late payment in the past year. Those figures suggest BNPL is no longer mainly a checkout option for discretionary items; for many households it has become a way to stretch weekly food and fuel spending across pay cycles.

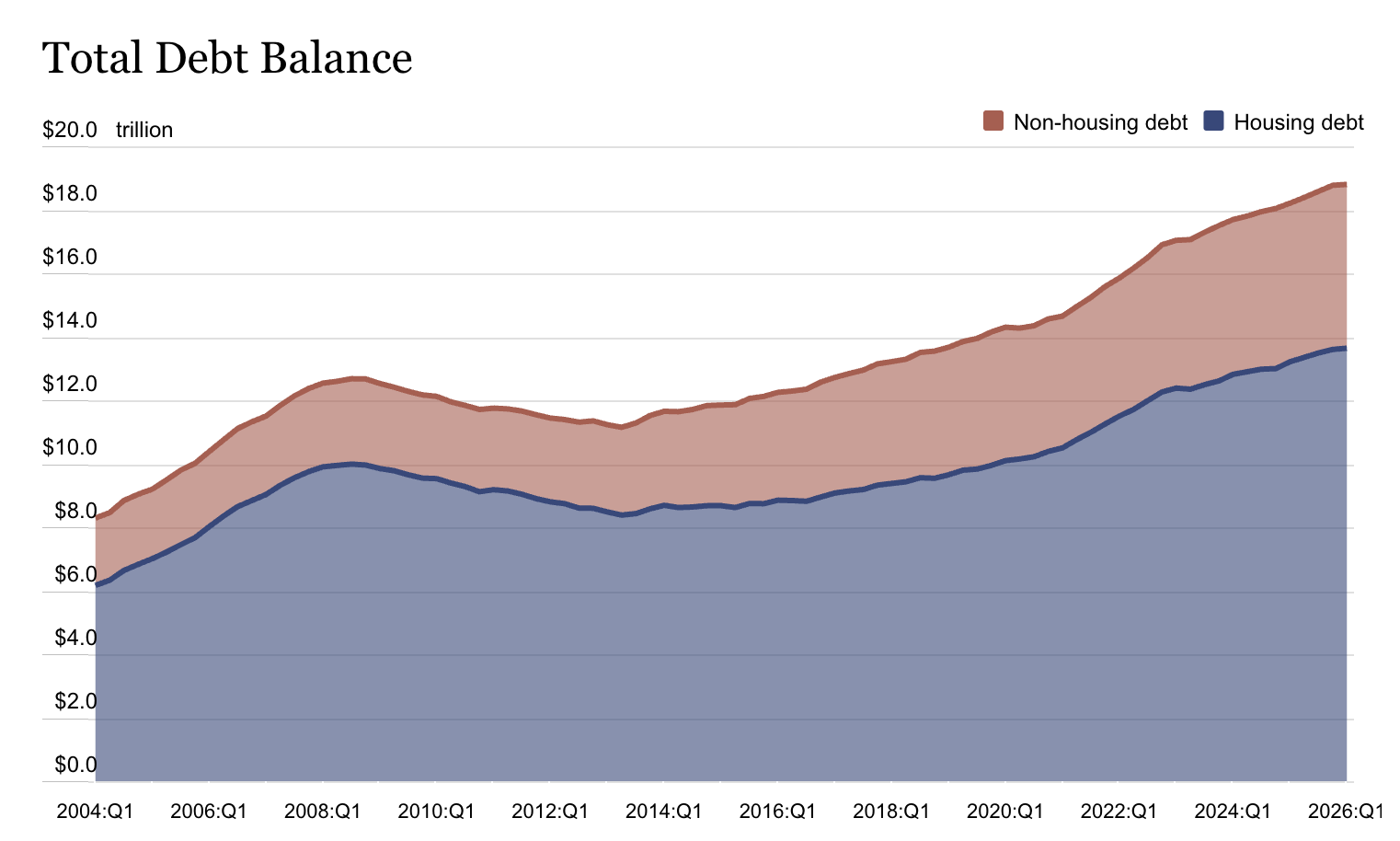

When consumers split a grocery run into four installments, it usually reflects a gap between income and living costs rather than a preference for financing. The Federal Reserve Bank of New York Quarterly Report on Household Debt and Credit shows total household debt rising $18 billion, or 0.1 percent, to $18.8 trillion in the first quarter, with aggregate delinquency little changed. As the chart below shows, that total-debt climb came as mortgage balances reached $13.19 trillion and transitions into early delinquency held steady for auto loans while ticking down for credit cards.

Source: Federal Reserve Bank of New York (Household Debt and Credit Report)

Regulators Are Watching Short-Term Credit at Checkout

The Consumer Financial Protection Bureau has tracked rapid growth in retail BNPL offers and the limited underwriting standards common in the products. For consumers, the convenience of splitting a $150 grocery bill can ease week-to-week cash flow, but missed payments can trigger fees when income is unpredictable. MarketWatch frames the trend as evidence of how expensive daily life has become, not as a neutral shift in payment preferences.

BNPL providers have expanded integrations with grocery chains and fuel retailers because high purchase frequency in those categories creates volume. Lenders gain visibility into recurring budget pressure that was harder to see when essentials were paid in cash or on debit alone.

The Risk of Financing Necessities Month After Month

Using installment credit for one-time purchases is different from using it for expenses that recur every week. Groceries and gas are not purchases a household can skip, which means a consumer who finances them in one cycle is likely to face the same gap in the next. That pattern can stack multiple open BNPL plans alongside rent and utilities. The personal saving rate fell to 2.6% in April, the lowest since before the pandemic, while PCE inflation ran at 3.8% year-over-year, leaving less room to absorb price shocks without borrowing.

Final Thought: When installment financing moves from want-based purchases to need-based ones like food and fuel, it reflects a structural cash-flow problem that payment flexibility alone cannot solve.