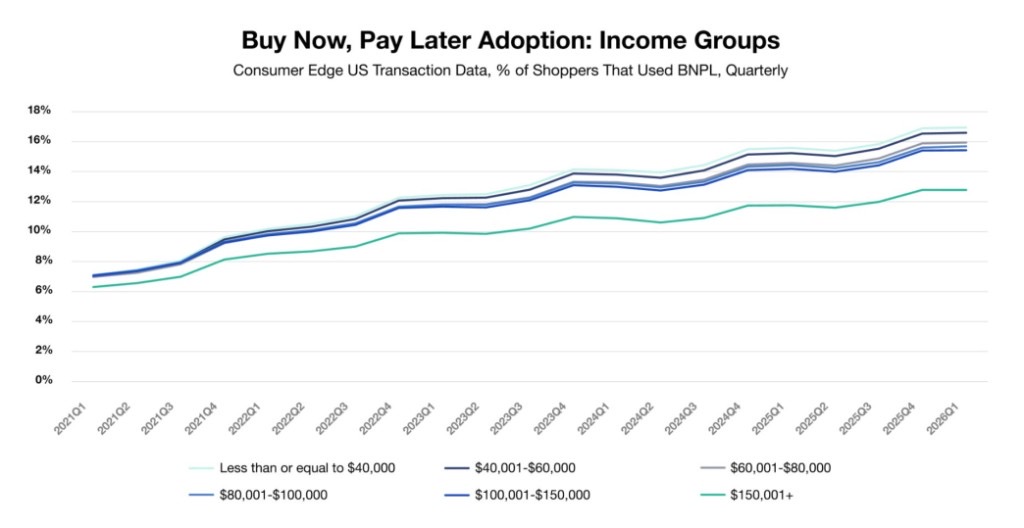

Buy now, pay later use more than doubled in the last five years, according to financial analyst Michael Gunther, who tracks spending data from 40 million credit and debit cards. Consumer Edge data shows adoption hit fresh highs in Q1 2026, with penetration climbing across every income group compared with a year earlier. That surge is happening as household budgets stay stretched and BNPL services become embedded in more online and in-store checkouts. Understanding the actual cost structure, and the credit consequences, matters more now than ever for families managing monthly expenses.

Source: Consumer Edge

How the Standard "Pay in Four" Plan Works

The most common BNPL format, as detailed by CBS News, is the "pay in four" plan. Shoppers pay 25% of the purchase price at checkout, then make three additional payments over the following weeks. Many of these plans are interest-free when payments are on time, which is a key part of their appeal. Lorelei Salas, former supervision director with the Consumer Financial Protection Bureau, described BNPL as a potentially useful budgeting tool, but only when used carefully. "Buy one thing and then don't use [BNPL] again until you finish paying," Salas said, noting that tracking multiple due dates falls entirely on the consumer.

Source: CBS News

The Real Risk: Stacking Plans and Missing Payments

The behavior Salas flags as most dangerous is called "stacking," running multiple BNPL plans simultaneously. Gunther's data shows the share of consumers using more than one plan, and in some cases two or three or more, has risen substantially alongside overall adoption. Each plan carries its own due dates, and missing any one of them triggers fees or other consequences that vary by lender.

Late fees differ across the major providers. Klarna charges up to $7 per missed payment, while Afterpay charges up to $8, with both capping fees at 25% of the purchase amount or less. Both companies send reminders and offer a 10-day grace period before applying the fee. Afterpay reported that as of May 2026, 98% of all purchases through its service incurred no late fee, suggesting most users do pay on time. Affirm takes a different approach: it charges no late fees at all, but a missed or late payment may result in the consumer being blocked from using the service for future purchases. Klarna and Afterpay similarly suspend new loan access for users who fall behind.

Credit Bureau Reporting Varies Widely

One of the most consequential differences among BNPL providers involves credit bureau reporting, an area where policies diverge sharply. According to CBS News, more BNPL services are now reporting to credit bureaus, which means payment behavior can follow a consumer financially. Affirm reports all loan activity to TransUnion and Experian on a monthly basis, though that activity is not currently factored into credit scores or visible to other lenders. Klarna does not report interest-free BNPL transactions in the U.S. but does report its interest-bearing, longer-term transactions to both TransUnion and Experian. Klarna also performs a soft credit inquiry for all products, which does not affect credit scores. Afterpay does not report any BNPL activity or account information to credit bureaus and conducts only soft credit checks.

The Consumer Financial Protection Bureau has tracked the rapid expansion of the BNPL market, including loan volume, user counts, and late fees across major providers, and the Federal Reserve Bank of New York monitors household debt trends that include the growing role of nonbank financial institutions such as BNPL providers in consumer credit markets. Both bodies have noted that the rise of nonbank lending creates new complexity for households trying to manage their overall debt picture.

What Households Should Watch Before Signing Up

The fee structure and credit reporting policies each company uses are not uniform, and reading the fine print before committing to a plan is the practical step experts emphasize. The 25% fee cap and 10-day grace periods at Klarna and Afterpay provide some protection, but stacking multiple plans removes much of the safety margin. Gunther's data from 40 million cards points to a consumer base increasingly reliant on installment tools that carry real financial consequences when mismanaged.

Final Thought: BNPL's doubling in five years reflects genuine budget pressure on U.S. households, but the patchwork of fee structures and credit reporting rules means the true cost depends heavily on which service you use and whether you keep every payment on time.