Bank of America Brings Installments to Credit Cards

Repayment windows ranging from three months to 18 months are now available to Bank of America credit card holders through a new feature called the Custom Pay Plan, the bank announced in a June 10 press release. Customers can activate the plan directly in BofA's mobile app or online banking platform after making a purchase on an eligible card, converting a standard charge into a structured installment schedule without applying for a separate loan or financing product.

The Custom Pay Plan is one of three features Bank of America introduced simultaneously, alongside a new loyalty rewards program and a credit monitoring service. Together, the announcements signal the bank's effort to compete more directly with the buy now, pay later tools that have grown rapidly outside traditional banking, as PYMNTS.com reports.

Source: PYMNTS.com

Why BofA Is Moving Now

The timing reflects a measurable shift in how Americans use financing at checkout. Research cited by PYMNTS Intelligence as of May 27 found that the availability of installment plans and merchant financing directly influences where consumers choose to spend. That influence is especially pronounced in categories where shoppers have time to compare options, including travel, food delivery, and experiences, while grocery and restaurant spending remains less affected because habit and immediacy still dominate those decisions.

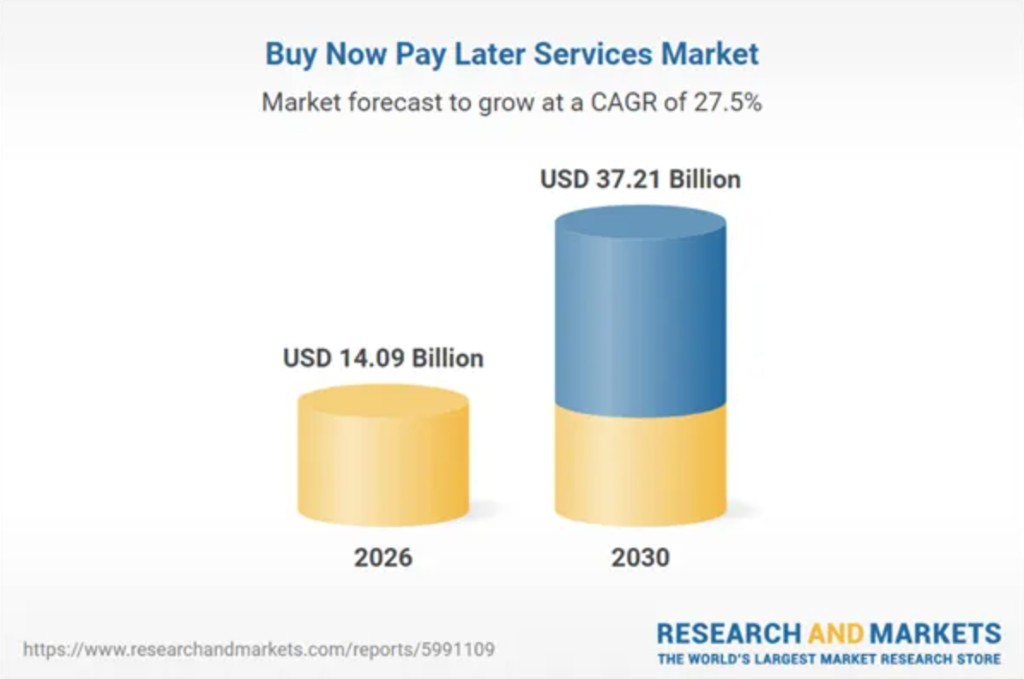

The broader buy now, pay later market underscores why banks are racing to keep pace. Industry research summarized by Yahoo Finance projects the global BNPL services market will expand from $10.87 billion in 2025 to $14.09 billion in 2026, at a compound annual growth rate of 29.6%, then reach $37.21 billion by 2030 at a 27.5% CAGR. That growth reflects increased online shopping, demand for payment flexibility, and wider adoption of alternative credit models. Key trends include tighter BNPL integration at checkout, AI-based credit assessments, and mobile-first platforms—patterns that the surge in e-commerce reinforces. The U.S. Department of Commerce reported retail e-commerce sales of $289.2 billion in Q1 2024, a scale that helps explain why installment options have become a competitive baseline for merchants rather than a niche checkout add-on.

The Consumer Financial Protection Bureau has documented a parallel rise in retailers offering BNPL directly at checkout, a trend that has accelerated across multiple retail sectors—from apparel and beauty into travel, groceries, and gas—putting traditional banks under competitive pressure to offer similar flexibility within their existing card products. By embedding installment options inside an account customers already carry, BofA is positioning the feature as a retention tool rather than a standalone product.

Source: Yahoo Finance (Research and Markets / GlobeNewswire)

Credit Monitoring and AI Round Out the Package

The bank also launched My Credit, a service that lets cardholders view their FICO score and receive alerts when that score changes, all without triggering a hard inquiry. Customers can additionally use Erica, BofA's AI-powered assistant, to retrieve their credit profile on demand inside the app. The combination of real-time score tracking and conversational AI access moves credit monitoring from a periodic check-in into a more continuous financial visibility tool.

Holly O'Neill, president of consumer, retail, and preferred banking at Bank of America, framed the three launches together: "Whether someone is just starting their financial journey with us or has been a client for years, we're committed to rewarding and empowering them each and every day."

What This Means for Household Budgets

For households managing irregular or large expenses, an in-app installment option on an existing card removes the friction of applying for a separate personal loan or store financing plan. The Federal Reserve Bank of New York's household debt data tracks how consumers are carrying and managing credit obligations, and that data provides important context: as balances rise across U.S. households, tools that give borrowers clearer control over repayment timelines carry real budgeting implications. A fixed installment schedule can make a large purchase more predictable month to month compared with revolving minimum payments.

The key variable for consumers will be the cost. Standard BNPL products from fintechs often advertise zero-interest short-term splits, while bank-based installment plans frequently carry fees or interest. BofA has not publicly detailed the fee structure for Custom Pay Plan, so cardholders will need to review terms before converting a balance.

Final Thought: Bank of America's move embeds installment flexibility inside an account millions of households already use, but the true value depends on fee terms the bank has yet to disclose publicly. Consumers comparing this to standalone BNPL apps should request the full cost breakdown before splitting any purchase.

Sources

- Pymnts: Bank of America Adds Installment Plans to Credit Cards

- Yahoo Finance: Buy Now Pay Later Services Industry Business Report 2026-2035

- Consumer Financial Protection Bureau — Buy Now, Pay Later: Market trends and consumer impacts (September 2022)

- Federal Reserve Bank of New York — Microeconomics