AI Is Changing How Americans Manage Money

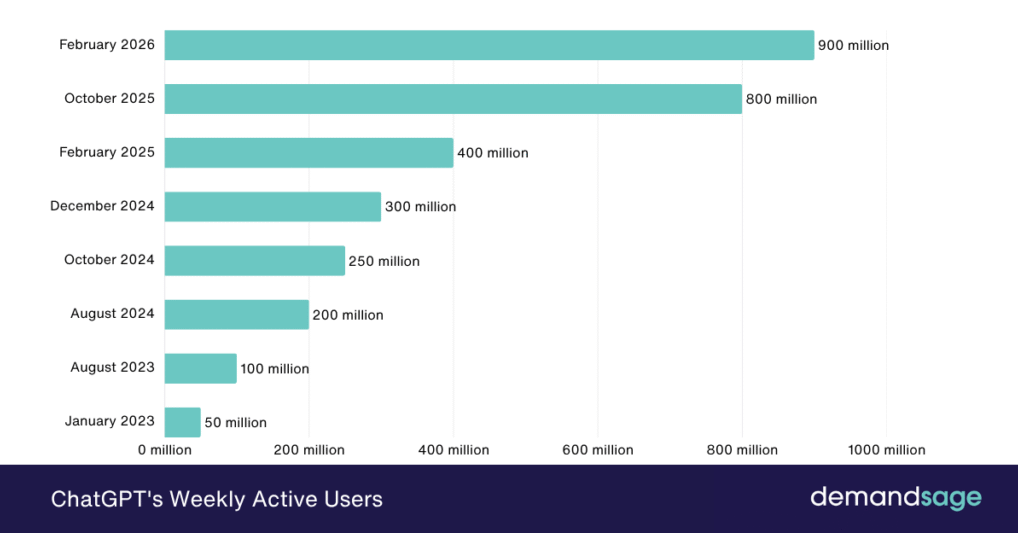

Artificial intelligence has moved quickly from novelty to a fixture in everyday financial life, powering budgeting chatbots, account-linking platforms, and automated spend trackers. Yahoo Finance reports that adoption is already widespread — and according to FNBO's 2025 Financial Wellbeing Study, 46% of Americans have used AI, such as ChatGPT, to help with their personal finances, with an additional 50% saying they trust AI for financial advice. That adoption is not surprising given how fast the underlying platforms have scaled. Sensor Tower estimates show ChatGPT crossed 1 billion monthly active users in May 2026, roughly three years after launch, faster than apps like TikTok, Instagram, and YouTube. As the chart below illustrates, weekly active users climbed from 50 million in early 2023 to 900 million by February 2026, putting mainstream AI assistants within reach of nearly any household with a smartphone.

Source: DemandSage (OpenAI, Reuters)

The core appeal is real. AI-powered apps can scan transaction histories, flag unusual charges, categorize spending automatically, and surface patterns a person might miss across dozens of accounts. For households juggling multiple bills, subscriptions, and variable income, that kind of automated analysis can save hours each month.

Yet as Yahoo Finance notes, the same tools that can simplify bill tracking and savings goals carry meaningful risks that households need to understand before handing over sensitive financial data.

Where AI Genuinely Helps With Household Budgets

The strongest use cases involve tasks that are repetitive, data-heavy, and low-stakes if a small error occurs. Categorizing grocery spending, flagging a subscription that renewed unexpectedly, or modeling how an extra $200 a month toward a loan affects payoff time are areas where AI tools perform reliably. Yahoo Finance points to AI-assisted platforms as alternatives to Mint (which was discontinued in 2024), where consumers seek automated budget tracking and bill organization without manual data entry.

The convenience factor is significant. Linking bank accounts and credit cards to an AI tool means real-time visibility into cash flow, which can be especially useful for couples managing shared expenses or anyone trying to build an emergency fund on a tight timeline.

Source: Pexels

The Risks: Data Privacy, Accuracy, and Over-Reliance

The benefits come with serious trade-offs. Sharing bank login credentials or granting broad data access to a third-party AI app creates privacy and security exposure. If an app is breached or sells data to partners, the household's complete financial picture, including account numbers, income patterns, and recurring bills, can be compromised.

Accuracy is a second concern. AI chatbots can generate confident-sounding answers about tax rules, loan terms, or credit score impacts that are simply wrong. Yahoo Finance has noted that consumers relying on AI-generated financial guidance without cross-checking authoritative sources risk making decisions based on outdated or fabricated information, a problem researchers sometimes call "hallucination." For a household deciding whether to refinance a mortgage or open a new credit line, a hallucinated interest rate or eligibility rule could be costly.

Over-reliance is a subtler danger. Delegating too much financial decision-making to an automated tool can erode the basic money literacy that helps people catch errors, negotiate better rates, or recognize when a deal is too good to be true. Certified financial planner Andrew Latham told Yahoo Finance that AI works best for exploring options and clarifying trade-offs, but final decisions should stay grounded in personal goals, risk tolerance, and common sense.

Practical Rules for Using AI Finance Tools Safely

The guidance from financial experts centers on a few concrete principles. First, treat AI as an analysis layer, not an advisor. Use it to surface data and flag patterns, then make decisions independently or with a licensed professional. Second, audit the permissions any app requests. Read-only account access is meaningfully safer than apps that request login credentials or the ability to move money. Third, verify any specific figure, rule, or recommendation an AI tool provides against a government source such as the Consumer Financial Protection Bureau or official lender documentation before acting.

Finally, households should review the privacy policy of any fintech or AI tool before linking accounts. Key questions include whether the company sells or shares transaction data, how long data is retained, and what happens to stored information if the company is acquired or shut down. Yahoo Finance recommends reviewing platform privacy settings, avoiding oversharing of personal details in chat prompts, and preventing apps from archiving conversations when that option is available.

Final Thought: AI can meaningfully reduce the friction of day-to-day money management, but the households that benefit most will be those who treat it as a starting point for financial decisions, not the final word.