Households Are Leaning More Heavily on Credit Cards

The Federal Reserve's Beige Book, a regular report of economic conditions gathered from businesses and contacts across all 12 Fed districts, is now sounding a clear note of concern about middle-income American households. According to Forbes, the latest edition warns of higher credit card usage and growing financial strain specifically among middle-income consumers, a segment that typically sits above eligibility for assistance programs but below the cushion of higher earners.

The Beige Book draws on qualitative reports from businesses, lenders, and community contacts, making it one of the broader real-world reads on how Americans are managing money right now. When the Fed's own survey network begins flagging credit card dependence in a specific income band, it reflects a pattern that lenders, retailers, and employers are all observing on the ground.

Source: Pexels

What Rising Credit Card Use Actually Signals

Credit card usage climbing among middle-income households is a different story than general spending growth. When people use cards to cover groceries, utilities, and other recurring bills rather than discretionary purchases, it typically signals that take-home pay and savings buffers are not keeping up with the cost of everyday expenses. The Forbes report frames this not as a spending splurge but as a financial strain indicator, meaning households are borrowing to bridge gaps rather than to buy extras.

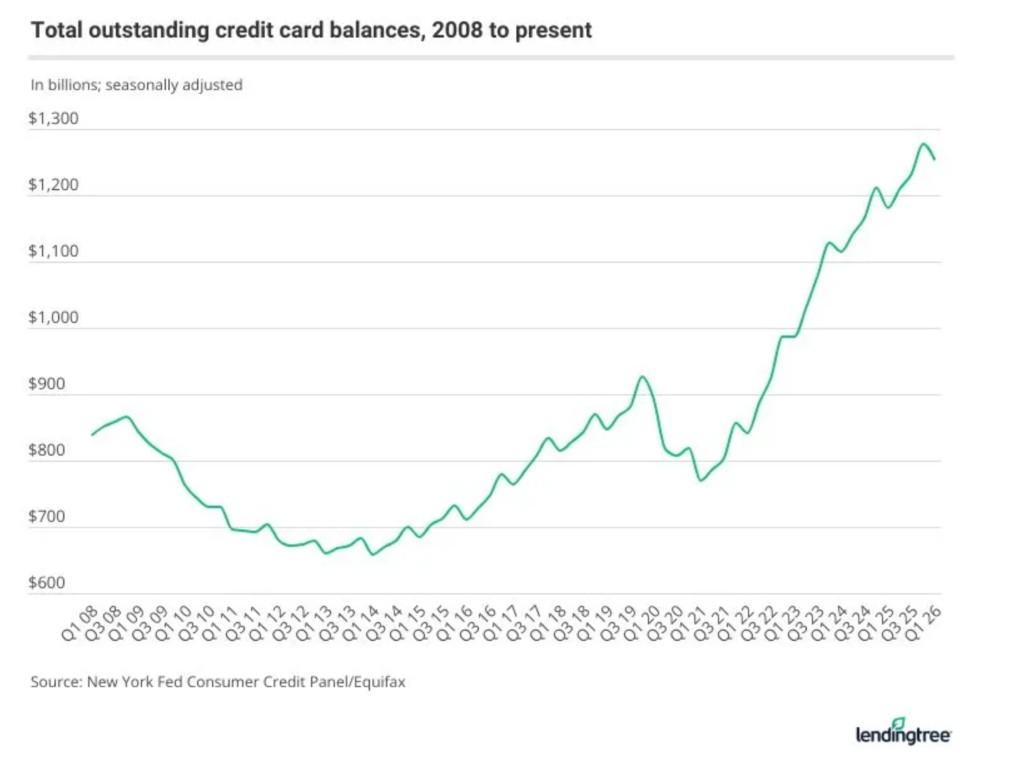

The aggregate numbers bear that out. Americans' total credit card balance stood at $1.252 trillion in the first quarter of 2026, according to LendingTree's analysis of Federal Reserve Bank of New York data — down slightly from a record $1.277 trillion in Q4 2025, but still $325 billion above the pre-pandemic peak of $927 billion set in late 2019. Since balances bottomed out at $770 billion in Q1 2021, total card debt has climbed 63% in five years. As the chart below shows, the hockey-stick growth that followed the pandemic-era dip has pushed outstanding balances to levels far above anything seen before 2023, when Americans first crossed the $1 trillion mark.

Source: LendingTree (2026 Credit Card Debt Statistics); data from the Federal Reserve Bank of New York Consumer Credit Panel/Equifax

This matters for budgets because credit card balances carry interest, and at current rates, carrying a balance from month to month accelerates how quickly a manageable shortfall becomes a compounding debt problem. The average APR on accounts that accrue interest was 21.52% in Q1 2026, according to the same LendingTree report, and roughly 45% of adult cardholders carried a balance for at least one month in the past year. A household that runs a balance to cover one month of tight expenses can find the following month harder to square, as the minimum payment itself crowds out room in the budget.

Why Middle-Income Households Are Particularly Exposed

Middle-income Americans occupy a difficult position in periods of financial stress. They generally do not qualify for income-based relief programs, and they are less likely to have large liquid savings or investment accounts they can draw on without penalty. As Forbes notes, this group is absorbing cost pressures, including persistent inflation in housing, insurance, and food, without the same safety nets available to lower-income households or the asset buffers available to higher earners.

The Beige Book's geographic reach, covering all 12 Federal Reserve districts, means the pattern is not isolated to a single region or city. When contacts across multiple districts report the same trend, it suggests the pressure is broad rather than localized.

What This Means for Household Budgets

The Fed's signal is a useful prompt for households to examine whether credit card charges are covering true discretionary spending or are filling gaps left by income that has not kept pace with bills. Understanding which expenses are being financed on credit, and at what interest rate, is the first step in assessing whether a budget gap is temporary or structural.

For households already carrying balances, the cost of that debt is itself a line item that grows unless it is actively reduced. The Forbes piece points toward consolidation and structured repayment strategies as approaches worth examining, particularly for middle-income earners who have steady income but are watching it absorbed by a growing list of obligations.

The Beige Book does not predict a crisis, but its warning about credit card usage among middle-income households is a concrete data point that the financial cushion many Americans relied on after the pandemic has thinned considerably.

Final Thought: The Fed's Beige Book rarely uses the word "strain" lightly, and its signal about middle-income credit card dependence is a sign that household budgets are under real, documented pressure, not just anecdotal stress.