Student Loans Makes the Major Choice a Budget Decision

Roughly 6.6 million student loan borrowers have become newly delinquent since the pandemic-era payment pause ended, according to Investopedia's analysis of federal repayment data. That backdrop makes the earning power of a chosen major less abstract: for households still carrying balances or co-signing loans, the first few years of post-college income largely determine whether monthly payments fit alongside rent, groceries, and savings.

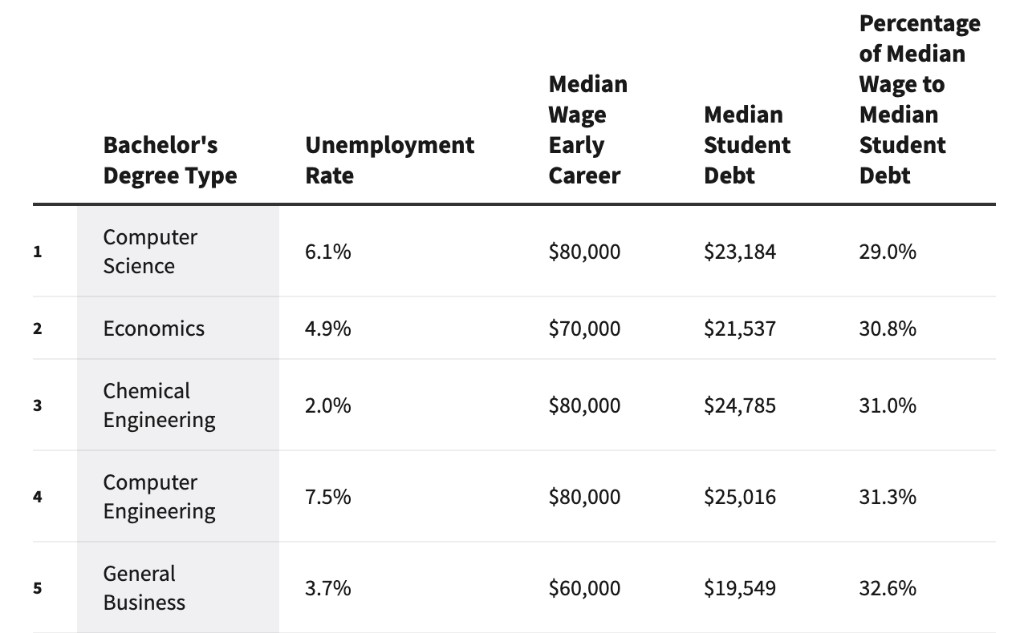

Against that pressure, Investopedia ranked bachelor's degrees by comparing median early-career wages from the Federal Reserve Bank of New York with typical student debt levels from the Education Data Initiative. The metric is straightforward: what share of a graduate's starting salary does their median debt represent? Lower percentages generally mean faster payoff timelines and more room in a household budget.

Source: Pexels

The Top Five Degrees for Fast Loan Payoff

Computer science leads the ranking. The median wage for a computer science graduate in their early career is $80,000, and they take out $23,184 in student loans on average, a debt-to-income ratio of 29.0%. Economics ranks second at a $70,000 median starting salary and $21,537 in typical debt (30.8%). Chemical engineering ties computer science on pay at $80,000 but carries $24,785 in median debt (31.0%). Computer engineering also posts an $80,000 early-career wage with $25,016 borrowed (31.3%), and general business rounds out the top five at $60,000 in pay against $19,549 in debt (32.6%).

Source: Federal Reserve Bank of New York and Education Data Initiative

The table reflects a pattern Investopedia highlights across technical and quantitative fields: starting salaries high enough to absorb typical borrowing without straining monthly cash flow. For a family stress-testing loan payments before enrollment, these paired wage-and-debt figures are among the most concrete inputs available.

Computer Science Leads, but the Job Market Has Tightened

The unemployment rate for computer science majors is currently 6.1%, according to Investopedia, higher than the 4.1% rate for all workers and the 5.2% rate for all recent college graduates. Houston Public Media cites Federal Reserve Bank of New York data showing computer engineering unemployment at 7.5% and computer science at 7.0% among recent graduates, even as early-career median wages in those fields remain among the highest of any major.

Investopedia notes that AI-driven hiring shifts have cooled entry-level tech demand, a tension worth weighing alongside payoff math. A degree that repays debt quickly on paper still requires landing the job that delivers that $80,000 starting salary. The ranking measures repayment potential, not a guarantee of employment in the first year out of school.

Where Payoff Takes Longest

At the bottom of Investopedia's ranking, theology and religion graduates earn a median early-career salary of $42,000 while carrying $38,722 in student debt, meaning debt equals roughly 92% of first-year wages. General education and social services degrees rank second and third from the bottom, largely because wages in those fields fall below the median for bachelor's degree holders overall, even when total borrowing is not dramatically higher than in technical majors.

The contrast with computer science is stark: the same $23,184 debt load that represents less than one-third of a CS graduate's starting pay can consume nearly a full year's earnings for a theology graduate. That gap shapes real household choices about deferring savings, leaning on income-driven repayment, or stretching repayment over additional years.

What This Means for Household Budgets

Student loan defaults have also climbed since collections resumed. The Federal Reserve Bank of New York estimates that roughly 1 million borrowers entered default in the fourth quarter of 2025 and another 2.6 million did so in the first quarter of 2026. CNBC reports that missed payments are concentrated among borrowers who were current before the pandemic, suggesting fresh budget strain rather than only legacy delinquencies.

For families choosing a major, the Investopedia ranking is a pre-enrollment stress test: match expected early-career pay to realistic debt levels before signing promissory notes, not after graduation when interest is already compounding. A degree's payoff speed does not dictate career passion, but it does set the monthly payment line item that competes with every other household expense for years afterward.

Final Thought: With millions of borrowers newly behind on payments and wide gaps between top- and bottom-ranked majors, matching a field's early-career salary to its typical debt load is one of the most consequential budget decisions a student and their family can make before college begins.

Sources

- Investopedia: Which College Degrees Pay Off Student Loans Fastest

- Federal Reserve Bank of New York — College Labor Market

- Federal Reserve Bank of New York — Federal Student Loan Defaults Return After Pandemic Pause

- CNBC: 2.6 Million Student Loan Borrowers Defaulted in Q1 2026

- Houston Public Media: AI and the Computer Science Job Market