AI Steps Into the Adviser Role

Chatbots built on large language models, including ChatGPT, Claude, and Google's Gemini, are now fielding the kind of personal finance questions that once required a paid human adviser, according to Bloomberg. Where a certified financial planner might charge several hundred dollars an hour, a chatbot subscription runs a fraction of that cost or nothing at all.

The shift is not hypothetical. An Intuit Credit Karma survey of 1,019 U.S. adults in August 2025 found that 66% of Americans who have used generative AI before say they use it to seek financial advice, rising to 82% of Gen Z and 82% of Millennials. Finance ranked as the second most common GenAI use case at 41%, just behind health and wellness at 44%.

The core appeal is accessibility. A household budgeting for the first time, navigating a job loss, or trying to understand loan options now has a conversational tool available at any hour. That convenience is driving real usage, and the financial services industry is paying attention.

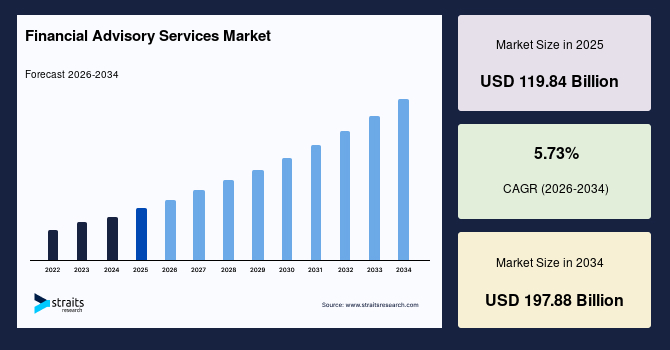

For technology companies, the opportunity is just as large. Financial advice sits inside a global advisory market that is already measured in the hundreds of billions of dollars and is still expanding. Straits Research estimates the global financial advisory services market was valued at $119.84 billion in 2025 and is projected to grow from $126.71 billion in 2026 to $197.88 billion by 2034, at a compound annual growth rate of 5.73% during the forecast period 2026 to 2034. As the chart below shows, that steady climb reflects rising demand for wealth management, retirement planning, and corporate restructuring. A chatbot that can answer even a slice of those questions at software scale is an attractive target for AI labs and fintech platforms alike.

Source: Straits Research

What These Tools Actually Do

According to Bloomberg's reporting, AI chatbots are handling tasks that range from explaining debt payoff strategies to walking users through insurance tradeoffs and savings planning scenarios. These are not simple keyword searches. The models can hold multi-turn conversations, remember context within a session, and produce tailored responses based on what a user shares about their income, expenses, or goals.

Credit Karma's survey data show how deeply users are integrating these tools into everyday money decisions. Among respondents who use GenAI for financial advice, the most common topics include financial education and basic personal finance concepts (35%), goal setting and action plans (35%), budgeting and expense management (34%), and investing in the stock market (32%). Nearly two-thirds (65%) say they seek financial guidance from AI often.

Many users also turn to chatbots for questions they would not ask a person. 75% of GenAI users say the tools let them ask financial questions they are too embarrassed to ask others. That helps explain why 85% of respondents who have used GenAI for financial advice say they have acted on the recommendations. Of those who acted, 80% say their financial situation improved because of GenAI, and 81% feel more confident managing their money. The capability gap between a chatbot and a licensed adviser has narrowed enough that some users are substituting one for the other entirely.

The Accountability Gap

Human financial advisers carry legal and regulatory obligations. They can be held to a fiduciary standard, face licensing consequences for bad advice, and carry professional liability. AI chatbots carry none of those obligations by default. If a chatbot steers a household toward a financial decision that turns out to be harmful, there is no clear recourse and no regulator currently overseeing that interaction the way FINRA or the SEC would oversee a registered adviser.

Andrew Lo, a finance professor at the MIT Sloan School of Management, told CNBC that the problem is not whether AI has enough financial expertise. "Clearly, AI has the expertise," he said. "What they don't have is that fiduciary duty. They don't have the ability to suffer consequences if they make a mistake to the same degree that a human advisor does."

Sebastian Benthall, a senior research fellow at New York University School of Law's Information Law Institute, framed the same tension as an open regulatory question: "Who's really responsible, and can people really be relying on a product to do this if it's not being backed up by a corporation with a fiduciary duty? It's really unresolved."

Bloomberg's coverage highlights this accountability gap as one of the central tensions in the rise of AI personal finance tools. The models can also hallucinate, meaning they may state figures, rules, or options with confidence that turn out to be incorrect. Lo noted that large language models "will always come back with an answer that sounds authoritative, even if it's not," and that AI is generally weak at number-heavy calculations involving taxes or a household's specific finances.

The picture is not simply AI versus trustworthy humans. Not all human financial advisers are fiduciaries, and legal duties vary depending on whether a consumer is speaking with a stockbroker, registered investment adviser, insurance agent, or other intermediary. Lo argued that government policy eventually needs to extend fiduciary protections to consumers who get financial advice from AI. Until then, households cannot fully delegate major money decisions to chatbots alone.

Credit Karma's data also show the limits of blind trust. 52% of respondents who acted on GenAI financial advice say they made a poor financial decision or mistake based on the information they received, even as 80% of those who acted report improved outcomes overall. Most users treat AI as a starting point: 80% say they still research and validate advice before taking action.

Source: Pexels

What It Means for Everyday Budgets

For most households, the practical implication is that free or low-cost AI guidance is now widely available and increasingly capable. Someone working through a debt consolidation question or trying to understand whether a high-yield savings account makes sense for their situation can get a detailed, personalized-sounding answer in seconds. That is a genuine democratization of access to financial information.

The caveat, consistent with Bloomberg's framing and the CNBC experts' warnings, is that these tools work best as a starting point rather than a final word. Users who treat chatbot output as verified advice from an accountable professional are taking on risk that the technology does not currently absorb on their behalf, and regulators have not yet fully addressed that gap.

Final Thought: AI chatbots are making financial guidance more accessible and affordable for everyday households, but the absence of fiduciary duty, the possibility of confident errors, and unresolved regulatory responsibility mean consumers are still the last line of quality control in that conversation.